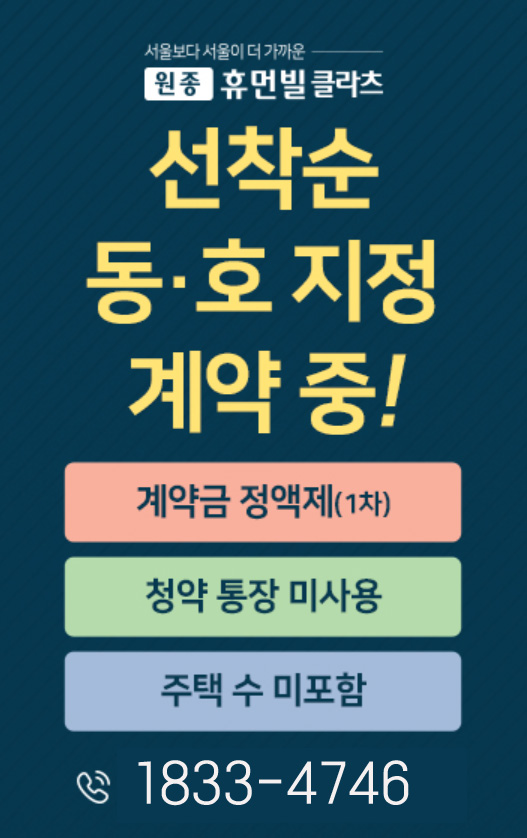

용인 남사 더클러스터

PREMIUM5

ONE&ONLY

용인의 정점이 될 단 하나의 주거공간

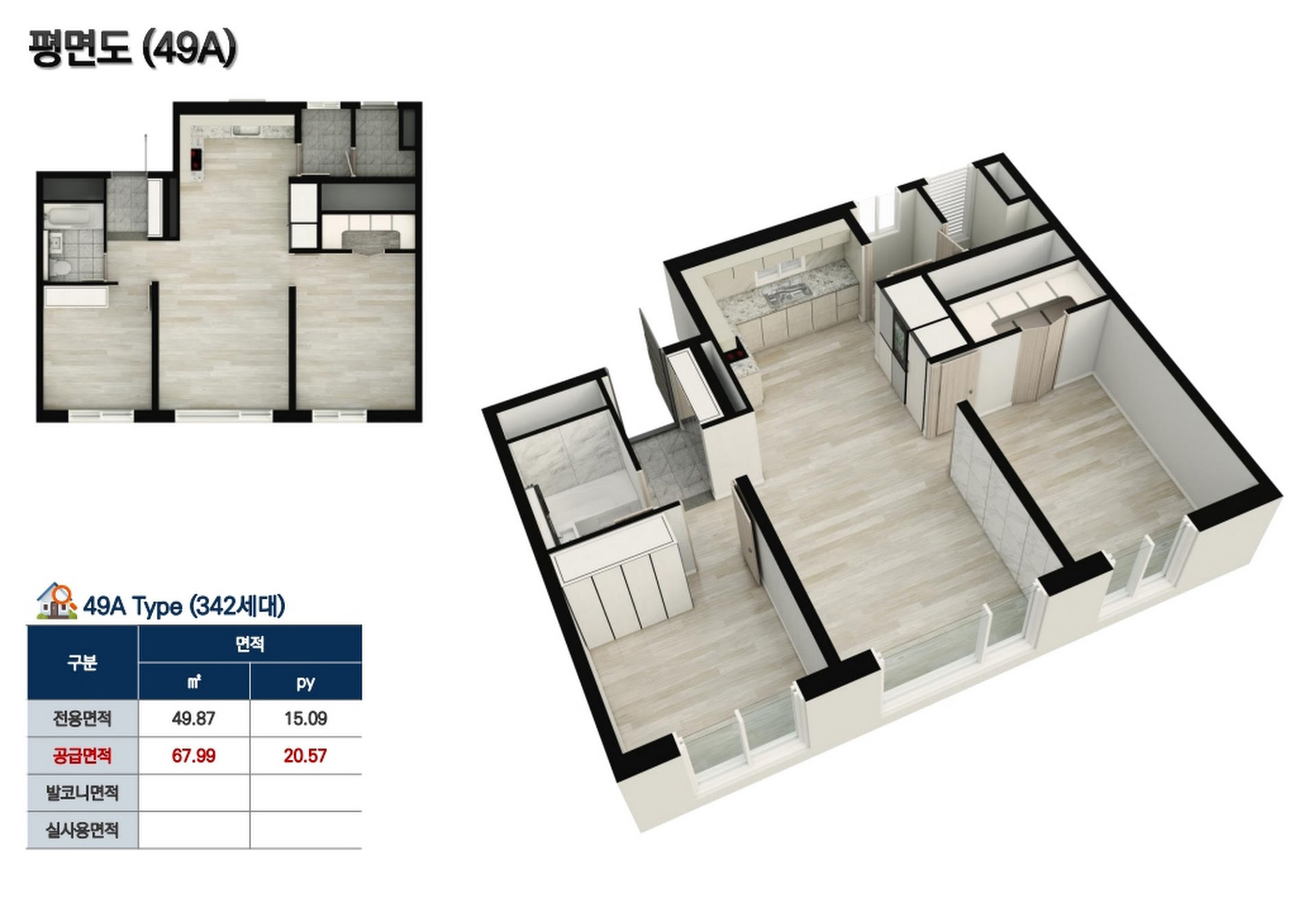

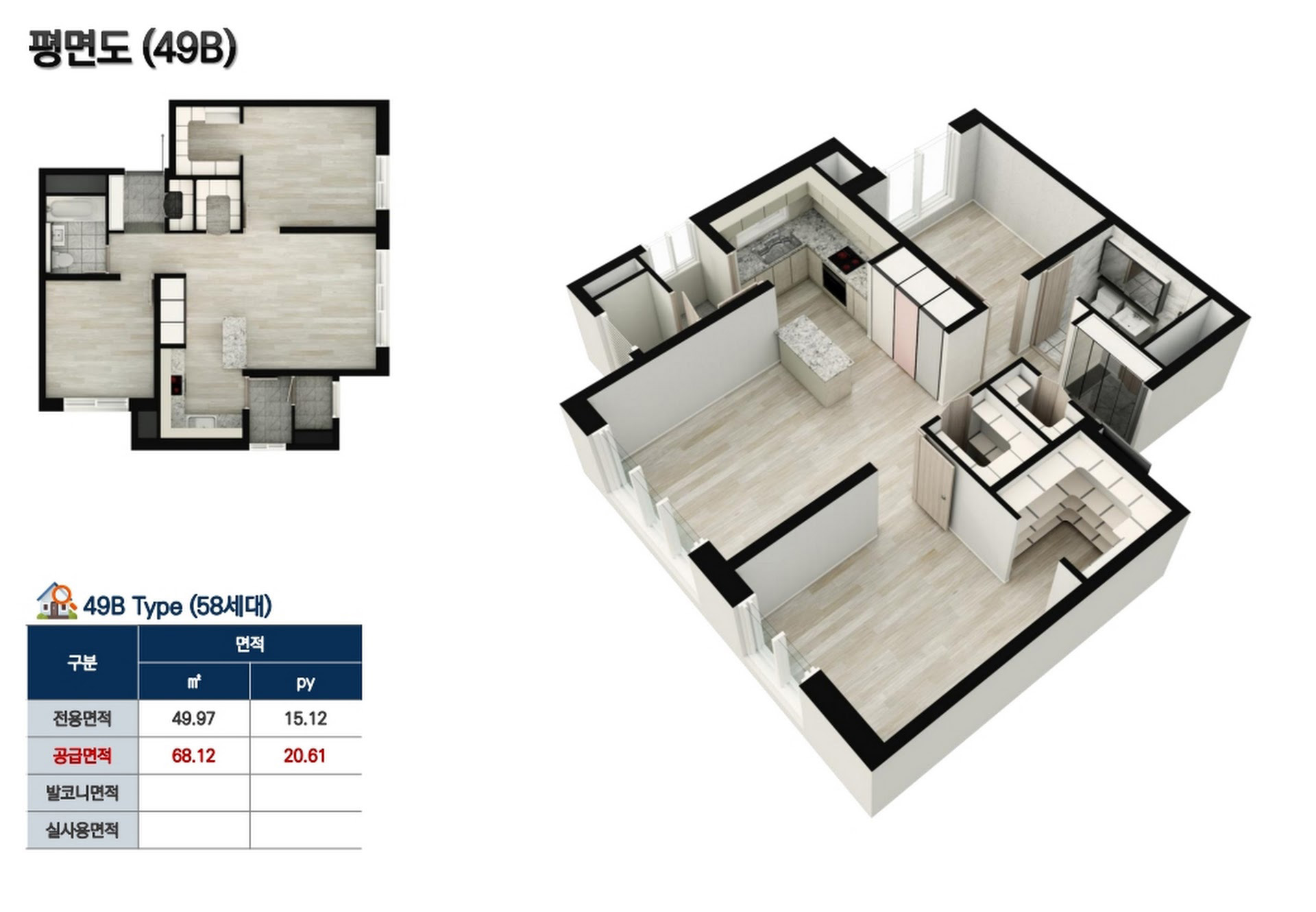

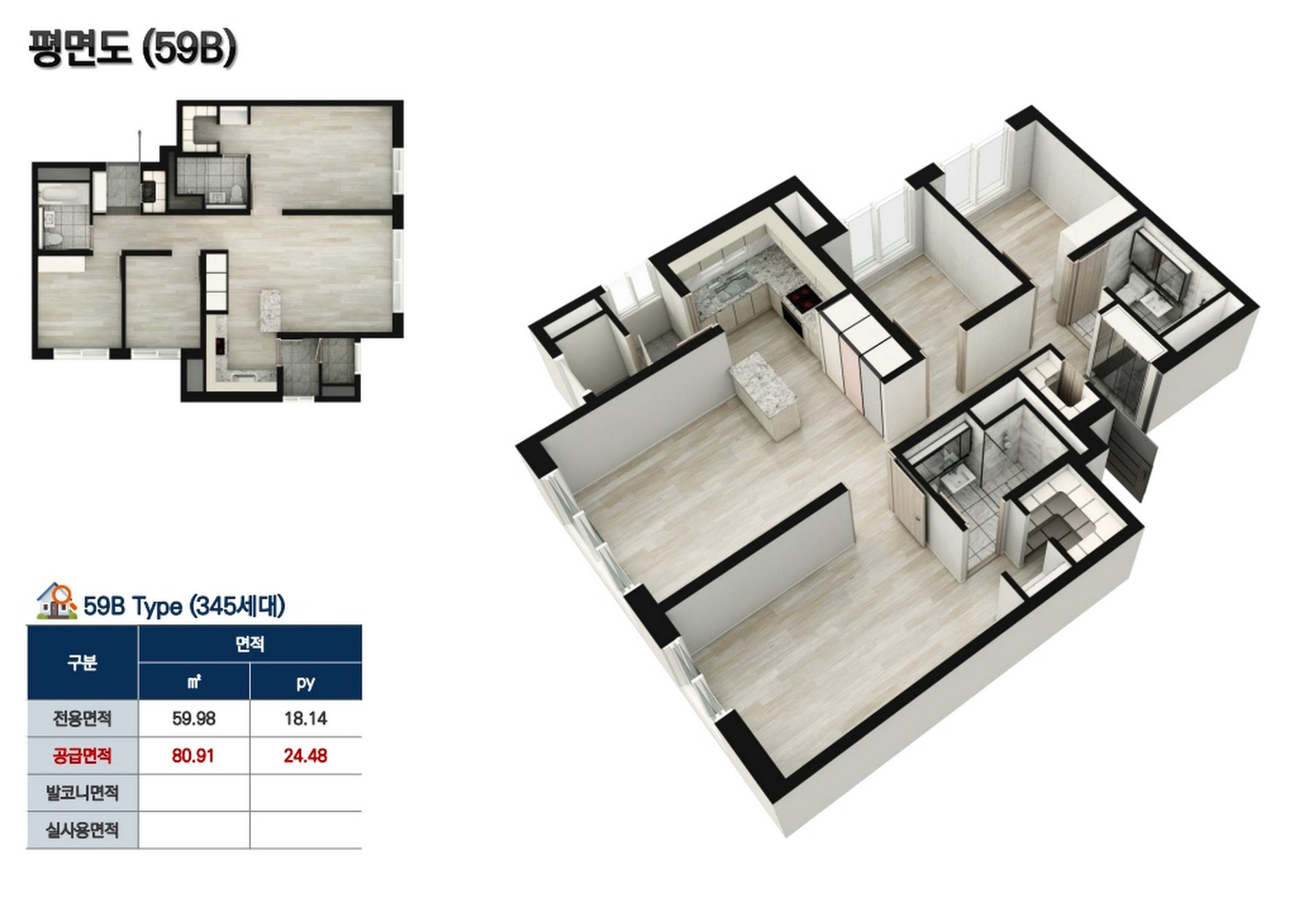

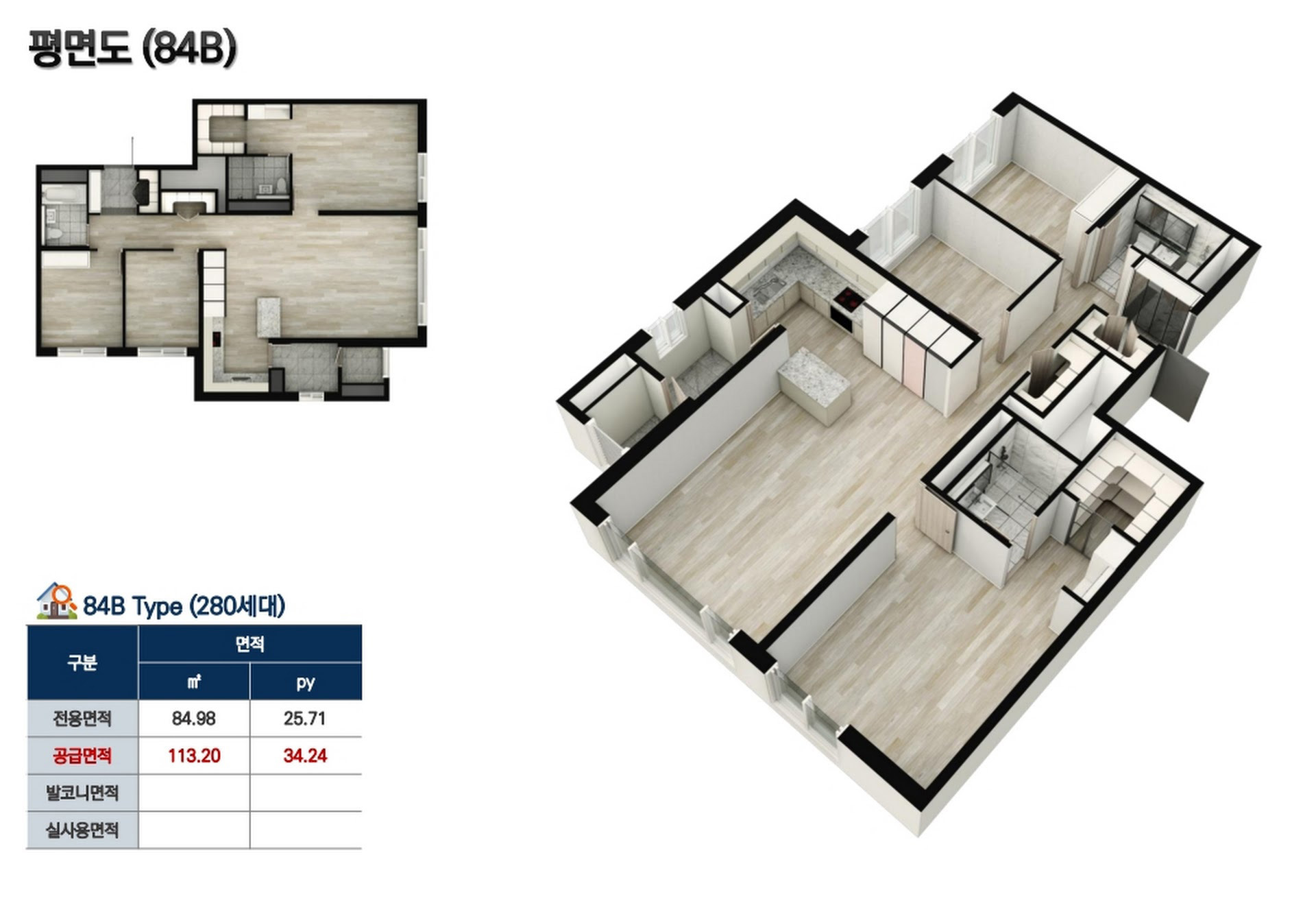

UNIT PLAN INFO

UNIT PLAN

DONGDAEGU STATION E-LIFE

Geographic

types

용인 남사 더클러스터

체크포인트

용인 핵심 랜드마크

- 10년간 임대 종료 후 분양전환 가능

- 청약통장 없이 누구나 청약 가능 (만 10세 이상)

- 주택수 상관 없이 신청 가능

- 무제한 전매 및 전대차 가능

- 취득세/재산세/종부세/양도세 없음

- 360조 투자확정 삼성 반도체 클러스터 1km 거리

Reservation

24시간 연중무휴

상담 운영중

문의하실 내용이

있으신가요?

궁금한 점이 있으시면, 언제든지 문의해 주세요. 우리는 고객의 질문에 빠르고 정확하게 답변하며 도와드리겠습니다.

CONTACT US

온라인 방문예약

문자 발송 안내

온라인 방문예약 접수를 해주시면

홍보관 주소가 문자발송 됩니다.

용인 남사 더클러스터

대표번호

☎1800-5743

대표 이메일

nxnxqx@naver.com

전화상담

전화상담